Menu

Back to Insights

Insights

17 November 2025

Sequencing Risk: A Quiet Threat to Retirement

Key Insights:

Sequencing risk occurs when poor market returns early in retirement combine with withdrawals, reducing how long savings can last.

The first few years of retirement are the most critical, as downturns during this period can permanently damage a portfolio.

Investors can manage sequencing risk by maintaining a cash buffer, diversifying investments, and adjusting withdrawals when markets fall.

Share

For many investors approaching retirement, the focus is often on how much they've saved. But there's another, less obvious factor that can dramatically affect how long those savings last: sequencing risk.

What Is Sequencing Risk?

Sequencing risk, also known as sequence-of-returns risk, refers to the significant impact that poor investment returns early in retirement, combined with regular withdrawals, can have on the longevity of a retirement portfolio.

Imagine two retirees with identical portfolios and withdrawal plans. If one experiences market downturns early in retirement and the other later, the first retiree may run out of money much sooner, even if both have the same average return over time. That’s sequencing risk in action.

Why Timing Matters

When you're working and contributing to your investments, market dips are often just bumps in the road. But once you retire and start withdrawing funds, those same dips can become potholes. If the market drops and you’re withdrawing money at the same time, you’re selling assets at lower prices, leaving fewer assets to recover when the market rebounds.

This is especially problematic in the first few years of retirement. A bad start can permanently damage your portfolio’s ability to support you over the long term.

Example: How Sequencing Risk Plays Out

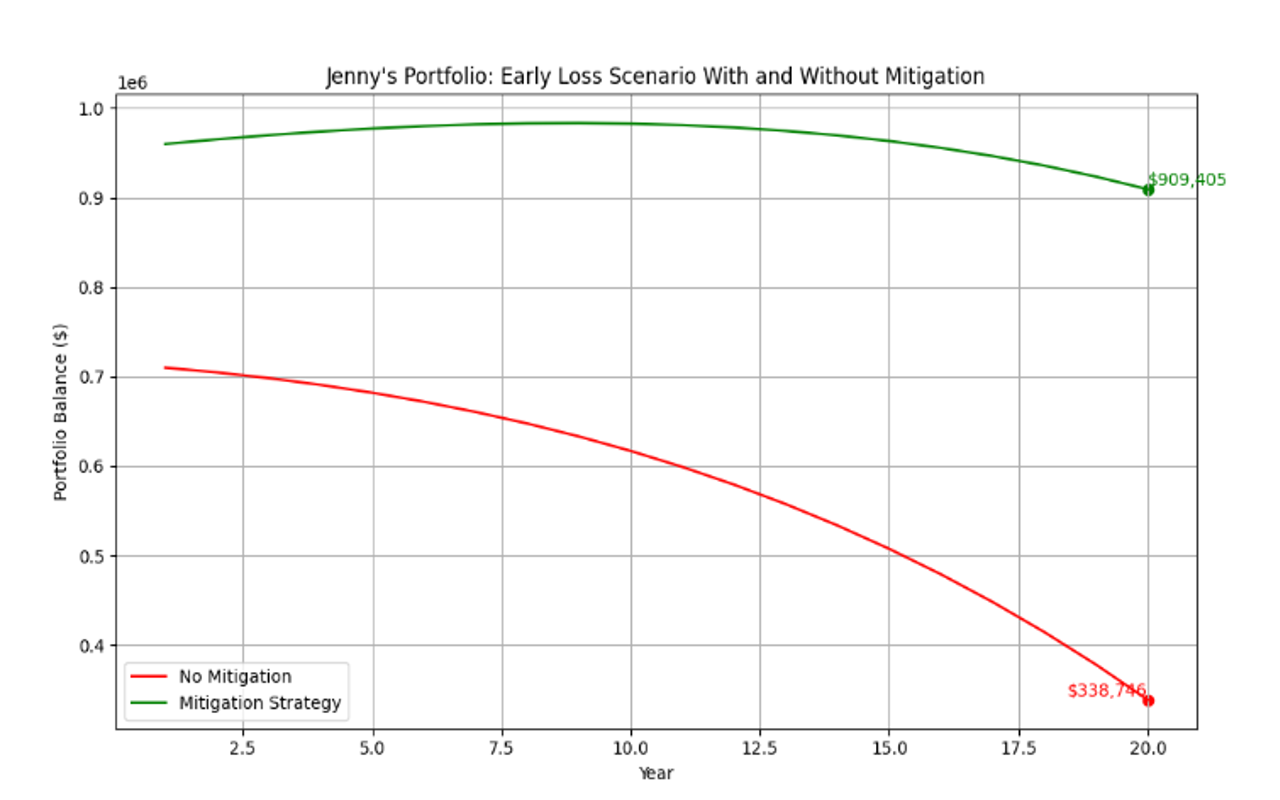

Imagine Jenny retires with $1 million and plans to withdraw $40,000 each year. If her portfolio grows in the first few years, she’s in good shape. But what if the market drops right after she retires?

Here’s what happens:

- Year 1: A severe downturn hits, and her portfolio loses 25%.

- She still withdraws $40,000, which now takes a bigger bite out of a smaller balance.

- Even if returns recover to +5% per year after that, the damage is done.

After 20 years, Jenny’s portfolio could end up $570,000 smaller than if the losses had occurred later as depicted in the chart below. That’s the power of sequencing risk, and why timing matters.

How to Manage Sequencing Risk

While you can’t control the market, you can take steps to protect yourself from sequencing risk:

- Build a cash buffer: Keep 1–2 years of living expenses in low-risk, liquid assets like cash. This lets you avoid selling investments during market downturns.

- Diversify your portfolio: A mix of stocks, bonds, and other assets can help smooth out returns and reduce volatility.

- Be flexible with withdrawals: If markets are down, consider reducing or delaying withdrawals to preserve capital.

- Tax efficient withdrawal planning: Sequence withdrawals from taxable sources first, then tax-deferred and finally tax-free sources (e.g. pension phase superannuation) to minimise tax drag and extend portfolio longevity.

Final Thoughts

Sequencing risk is a subtle but powerful force that can derail even well-planned retirements. By understanding it and preparing accordingly, investors can better protect their financial future and enjoy retirement with greater peace of mind.

Contributions from

No items found.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Related

No items found.